The price of every stock practically changes every second.

Let’s go into a Thought Experiment…

Imagine you open the trading app on your mobile and the stock that you purchased yesterday at ₹100.

₹101…₹103 – the stock starts moving upwards. Your optimism keeps rising as the price moves higher. ₹105…₹106 – now, you start feeling in control. You do not want to take your eyes off your investment, as you get satisfaction of seeing your decision turning out to be fruitful. But this lasts only for a brief while.

₹104…₹103 - the stock starts moving downwards. You feel a sense of loss – a sense of defeat. You start thinking that you could have sold it at ₹106. This pain of loss takes a toll on your mind despite staying in profit. At this moment, you want to do something – you feel an urge to act.

The surge in new Demat Accounts – with over 1.7 crore new account openings in the last 3 years – shows the extent of investor interest in stock trading. Moreover, as access to good technology is increasing, it is becoming easier for investors to frequently monitor their portfolios.

Markets behave irrationally, but why do we?

The principle of loss aversion posited in “Prospect Theory” developed by Richard Thaler and Amos Tversky states that people perceive losses disproportionately more negatively than they feel positively about gains of similar magnitude. This aversion can cause investors to prematurely sell off fundamentally strong stocks to minimise losses in the near term.

Various news and events impact the equity markets in the short term. Frequently checking your portfolio adds fuel to the fire as it could trigger you to make irrational decisions, making it counterintuitive to wealth creation.

An Example:

As per a January 2023 paper (Analysis of Profit and Loss of Individual Traders dealing in Equity F&O segment), published by the Securities and Exchange Board of India (SEBI), 89% of individual traders in the equity Futures and Options segment incurred losses, with an average loss of ₹1.1 lakh during FY2022, whereas, 90% of the “active” traders incurred average losses of ₹1.25 lakh during the same period.

The “active” trader tends to check his or her portfolio multiple times during the day and acts accordingly. Although traders aiming for quick profits often face significant challenges, as illustrated above, building long-term wealth necessitates distancing oneself from the noise that can create chaos in equity markets.

What is a “Good” Investment Horizon – 5 years, 10 years… or longer?

If you had invested your money from November 1993 to March 2003, the return (CAGR) on your investments would have been negative: -1%!

According to a publicly available study published in 2023 examining the price patterns of BSE Sensex over the previous 20 years, it was understood that out of the 4,971 trading days, less than 10% of the days (445 days) contributed to the Index’s 13-fold rise!

This information and the above chart imply that patience is a much-needed virtue to help you stay invested to navigate through different phases of the market and see your money compound in the long-term.

“Making your money work” – What does this mean?

It has often been stated and is considered that a Systematic Investment Plan (SIP) is an ideal route to wealth creation. The reason behind the same is that the periodic auto-debit of instalments allows you to stay disconnected from the noise surrounding the markets, which reduces your instinct to check your portfolio frequently.

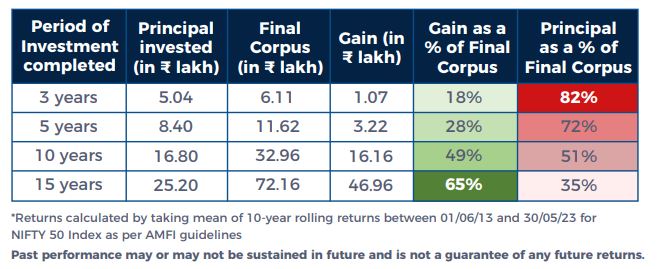

Furthermore, with a reduced propensity of redeeming your investments, there is a higher probability of you “making your money work” as the gains on your investment could become a higher proportion of your final value of the investment. The table below illustrates the same:

Assume you invested ₹12,000 per month in an equity fund. At the end of 15 years, at a rate of returns of 12.93%*, the gain as a % of your final corpus would be over 65% of the final corpus, while the principal invested as a % of your final corpus would be just 35%!

Hence, instead of checking your portfolio frequently, you may want to start counting the number of days stayed away from checking it, to enjoy a relatively smoother compounding journey.

It is so imperative to stay focused, stay disciplined and let your money work for you. Let’s spread the message to people who have tendency to check the wealth frequently.

Warm regards,

Tejas Lakhani, chartered accountant and a finance professional.

The information herein is for general purposes only. The recipient(s) should before taking any decision, make their own investigation and seek appropriate professional advice.

MUTUAL FUND INVESTMENTS ARE SUBJECT TO MARKET RISKS, READ ALL SCHEME RELATED DOCUMENTS CAREFULLY.